Light

Dark

If you're thinking about taking out a loan, one of the most important factors to understand is interest rates. They directly influence how much you’ll pay each month and how much the loan will cost you over time.

From home mortgages to credit cards, interest rates affect nearly every form of borrowing. But how exactly do they work — and why do they change?

Let’s break it down in simple terms.

An interest rate is the percentage a lender charges you for borrowing money. It’s essentially the cost of using someone else’s funds.

For example:

If you borrow $10,000 at a 5% interest rate,

You’ll pay 5% of that amount annually (depending on the loan structure).

Interest is usually expressed as an Annual Percentage Rate (APR), which includes the base rate plus additional fees.

When interest rates rise, borrowing becomes more expensive. Your monthly payments increase because a larger portion of your payment goes toward interest rather than the loan principal.

For example:

A $250,000 mortgage at 3% interest costs significantly less per month than the same loan at 7%.

Even a 1–2% difference can mean paying tens of thousands more over the life of the loan.

When rates are low:

Monthly payments decrease

Total repayment cost drops

Borrowers can qualify for larger loan amounts

This is why many people refinance when interest rates fall.

Interest rates don’t just affect monthly payments — they affect the total cost of your loan.

Let’s say you take out a 30-year mortgage:

At 3%, you might pay $150,000 in interest.

At 6%, you could pay over $300,000 in interest.

That’s double the cost — just from a rate change.

Stay the same for the entire loan term

Provide predictable monthly payments

Ideal when rates are low

Change over time

May start lower than fixed rates

Can increase if market rates rise

Choosing between them depends on your financial stability and risk tolerance.

Interest rates are influenced by several factors, including:

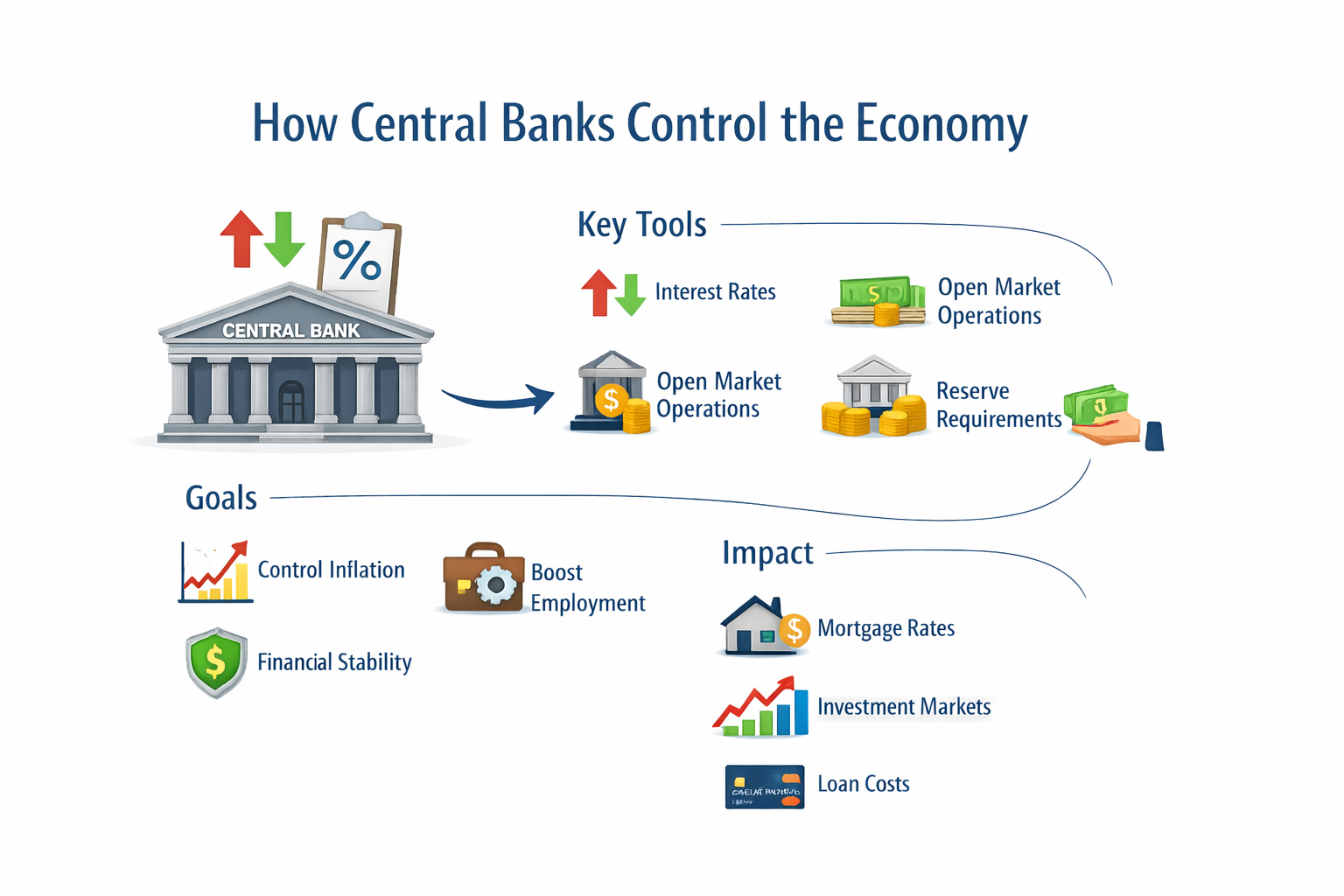

Central bank policies

Inflation

Economic growth

Supply and demand for credit

Global financial conditions

When inflation rises, central banks often increase interest rates to slow spending. When the economy slows down, they may lower rates to encourage borrowing and investment.

Higher rates reduce home affordability and increase monthly mortgage payments.

Rising rates can increase car financing costs, affecting your budget.

Unsecured loans often have higher interest rates, especially if your credit score is low.

Most credit cards have variable rates, meaning your interest charges can rise quickly when rates increase.

Here are smart financial moves to consider:

✔ Improve your credit score to qualify for lower rates

✔ Compare lenders before applying

✔ Consider refinancing when rates drop

✔ Choose shorter loan terms when possible

✔ Avoid borrowing more than you can afford

Planning ahead can save you thousands.

Interest rates might seem like small percentages, but they have a powerful impact on your financial future. Whether you’re buying a home, financing a car, or taking out a personal loan, understanding how interest rates affect loans helps you make smarter decisions.

Before signing any agreement, always calculate:

Monthly payments

Total repayment cost

Long-term financial impact

A small rate difference today can mean big savings tomorrow.