Light

Dark

Understanding how central banks control the economy is essential for anyone interested in finance, investing, or economic policy. Central banks play a powerful role in shaping economic growth, controlling inflation, and maintaining financial stability.

When the economy grows too fast or slows down too much, central banks step in using specific tools to restore balance. Their decisions influence interest rates, loan affordability, employment levels, and even stock market performance.

But how exactly do central banks manage such a complex system? Let’s break it down in simple terms.

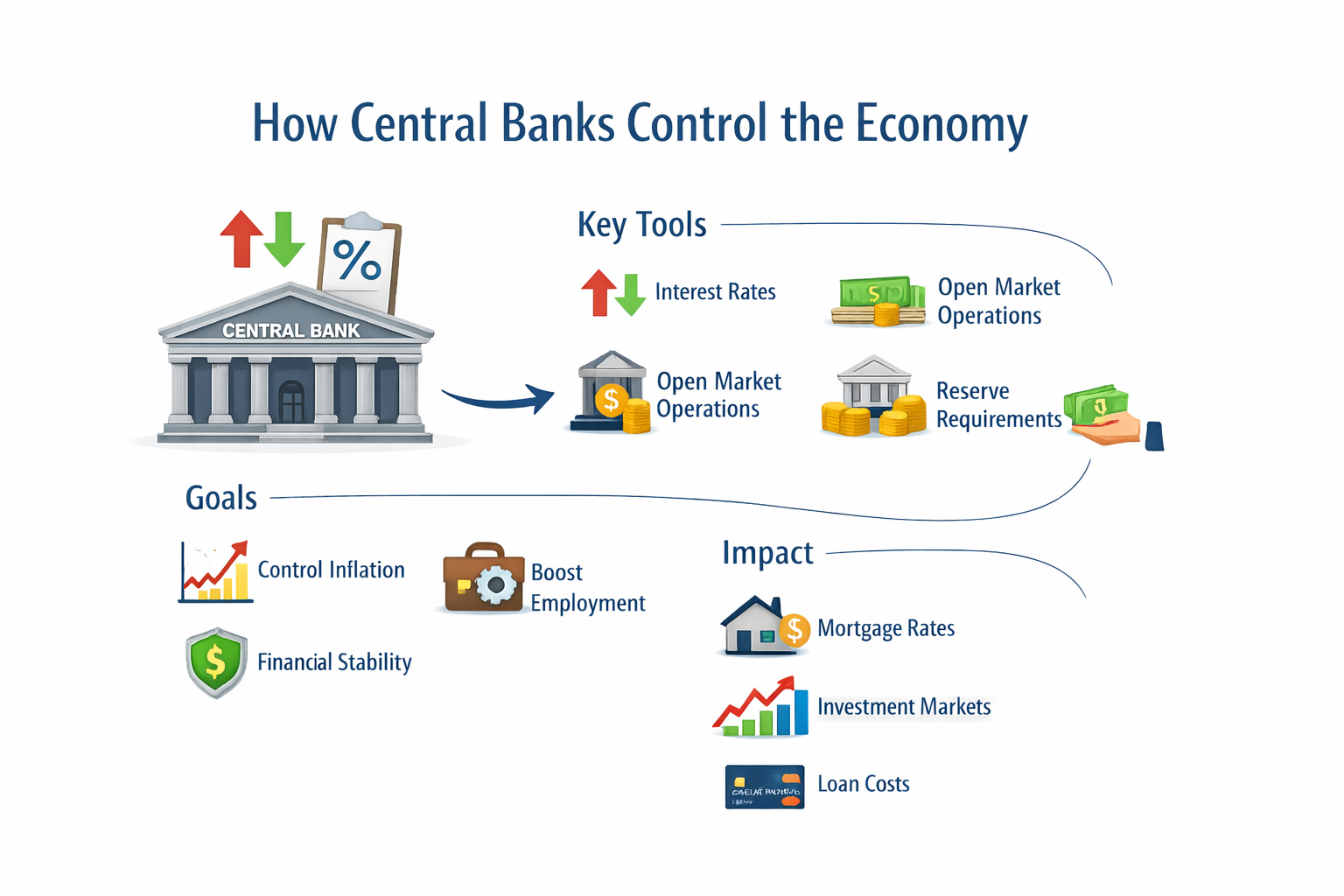

A central bank is a national institution responsible for managing a country’s monetary system. It regulates the money supply, sets interest rates, and supervises financial institutions.

Unlike commercial banks, central banks do not serve individual customers. Instead, they serve governments and the broader financial system.

Their main goals typically include:

Controlling inflation

Supporting employment

Maintaining price stability

Ensuring financial system stability

Central banks rely on monetary policy to influence economic activity. Here are the primary tools they use.

Interest rates are the most powerful tool central banks use to control the economy.

When inflation rises too quickly, central banks increase interest rates. Higher rates make borrowing more expensive, which slows consumer spending and business investment.

When the economy slows down, central banks lower interest rates. Lower rates encourage borrowing, spending, and investment, which stimulates economic growth.

Even small changes in interest rates can significantly impact mortgages, personal loans, and business financing.

Open market operations involve buying or selling government bonds in financial markets.

When a central bank buys bonds, it injects money into the economy.

When it sells bonds, it removes money from circulation.

This directly influences the money supply and short-term interest rates.

Central banks set reserve requirements, which determine how much money commercial banks must hold in reserve.

If reserve requirements increase, banks have less money to lend. This slows economic activity.

If reserve requirements decrease, banks can lend more, boosting economic growth.

Although this tool is less frequently adjusted today, it remains an important control mechanism.

Quantitative easing is used during severe economic downturns.

In this strategy, central banks purchase large amounts of financial assets to increase liquidity and stimulate lending. This approach was widely used during global financial crises and economic recessions.

Quantitative easing helps lower long-term interest rates and support financial markets.

Inflation control is one of the primary reasons central banks intervene in the economy.

If inflation rises too quickly:

Purchasing power declines

Living costs increase

Economic uncertainty grows

To combat inflation, central banks typically raise interest rates to reduce spending and borrowing.

On the other hand, if inflation is too low or deflation occurs, central banks lower rates to encourage economic activity.

Maintaining stable inflation helps create predictable economic conditions.

Central banks indirectly affect employment through their control of economic growth.

Lower interest rates encourage businesses to invest and expand. Expansion often leads to hiring more workers.

Higher interest rates may slow hiring but can prevent the economy from overheating.

Balancing inflation and employment is one of the most challenging tasks central banks face.

Central bank policies affect everyday financial decisions, including:

Mortgage rates

Credit card interest rates

Car loan costs

Savings account returns

Investment performance

When a central bank announces a rate change, financial markets react almost immediately.

Understanding how central banks control the economy can help you make smarter financial decisions and prepare for economic shifts.

While central banks aim for stability, their policies are not without criticism.

Common concerns include:

Delayed policy impact

Risk of triggering recessions

Asset bubbles caused by prolonged low rates

Political pressure influencing decisions

Monetary policy takes time to affect the economy, which makes timing extremely important.

Modern economies are more interconnected than ever. Global trade, digital currencies, and financial technology continue to reshape how central banks operate.

Emerging trends include:

Digital central bank currencies (CBDCs)

More data-driven policy decisions

Increased global policy coordination

As economies evolve, central banks must adapt their tools and strategies to maintain stability.

How central banks control the economy comes down to one central principle: managing the money supply and interest rates to maintain balance.

By adjusting interest rates, conducting open market operations, and using tools like quantitative easing, central banks influence inflation, employment, and overall economic growth.

Their decisions shape the financial environment we live in every day. Understanding these mechanisms allows individuals and businesses to better navigate economic cycles and plan for the future.

The main role of a central bank is to maintain economic stability by controlling inflation, regulating the money supply, and supervising the financial system.

Central banks typically raise interest rates to reduce borrowing and spending, which helps slow inflation.

Lower interest rates encourage borrowing, spending, and investment, which stimulates economic growth.